For bonds acquired on the secondary market, that we may want to sell before maturity, the intrinsic price calculated by adding face value and accrued interest doesn’t reflect the actual street price of the bond that we would receive when selling it.

Apart from connecting a data feed that contains current market prices for the bond, there could be an option to provide manual prices instead of the one calculated by the model.

If that option would be enabled, automatically calculated prices would be ignored and only the manual prices would be used. The interest calculation model would only be used to create coupon payouts and maturity event

hi that would solve that big problem of not having bond feed for the UK and a few other places, I think US too. You could put in an indicator that prices are manual.

I think ideally you could display

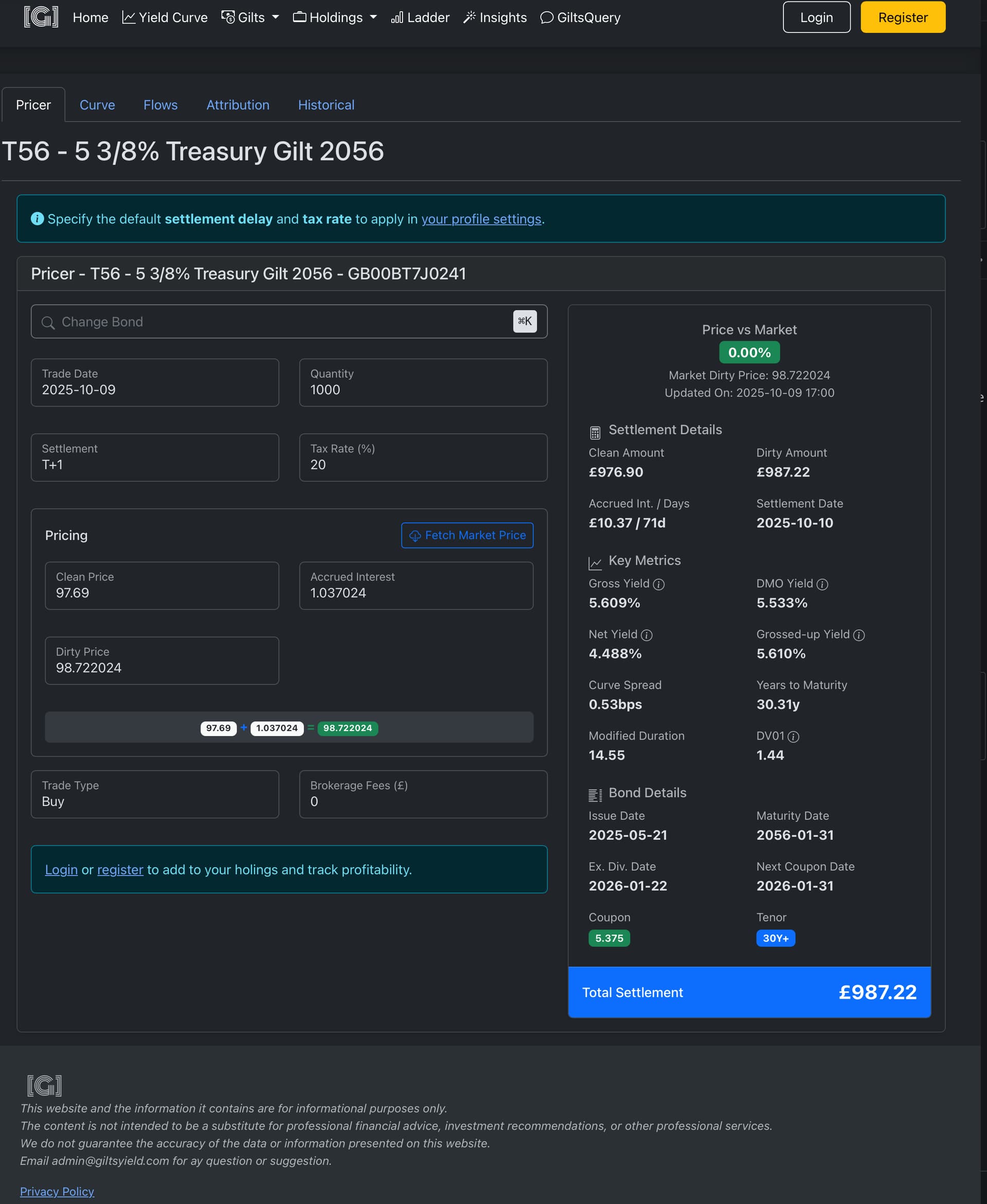

1 Clean Price - quoted price

2 Dirty Price (clean + accrued interest to next coupon) which is the price you really would pay to buy it

3 Accrued Interest

4. if you then had the total coupons remaining to maturity and the % return if held to maturity I think that covers every angle.

With that and your charting ability in Capitally you could see bond ladders very nicely. I don’t think there are many portfolio tools out there that can do this